Authors: Jingjing Qian, Jia Yang

The concept of green finance has emerged in recent years as an important way of supporting sustainable and low-carbon development. It is entering the mainstream of global financial community. Green finance refers to those financial instruments and investments that can result in environmental benefits, such as loans for environmental protection and clean energy projects, bonds for pollution control infrastructure, and special funds for supporting green industries. The environmental benefits also include the protection of natural and global climate systems. Such benefits must be real, verifiable, and additional to the normal effects that conventional financial activities would cause. Climate finance is part of green finance specifically referring to the financial instruments and investments that aim to reduce greenhouse gas emissions (GHGs). Climate finance is an important tool for climate mitigation and expanding climate finance is the most urgent task of green finance, as we will explain below.

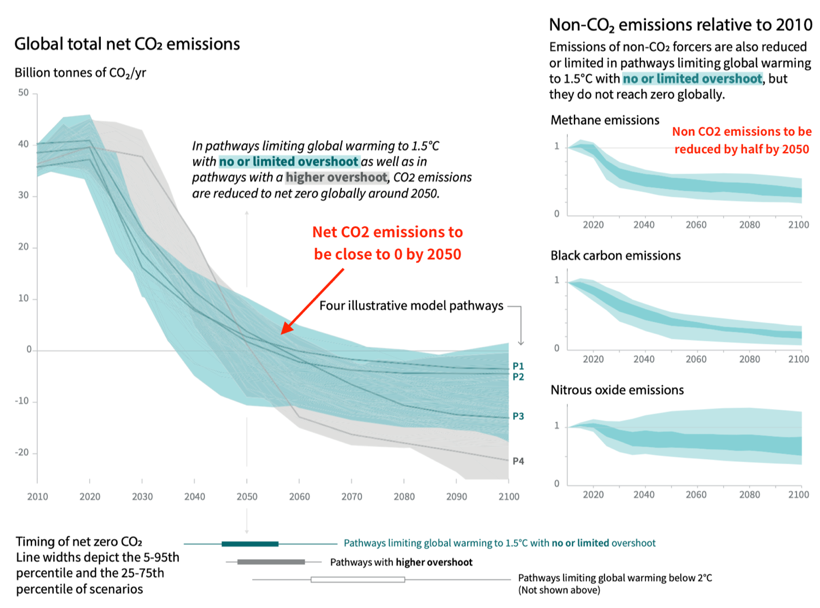

IPCC’s latest special report, Global Warming of 1.5 °C [1] (October 2018), emphasizes an urgent need to enhance and expand climate finance. Authored by nearly 100 world’s top experts and peer reviewed by nearly 500 scientists, this report concludes that the Earth's average temperature has already increased by 1 ℃ since the Industrial Revolution and that limiting the warming to 1.5 ℃ -2 ℃ by the end of this century is possible but would require "deep emissions reductions" and "rapid, far-reaching and unprecedented changes in all aspects of society” to avoid catastrophic impact of climate change. This means that by the middle of this century the global net CO2 emissions need to go down to zero and other GHGs (CH₄, N₂O, HFCs, etc.) need to be cut by half or more than their current levels, , as shown in Figure 1.

Figure 1 IPCC Special Report: Global Warming of 1.5 ºC on GHGs scenarios

The IPCC examined a variety of models of pathways to the 1.5 ° C warming limit and the respective costs. It has found that from 2016 to 2035, the world needs an average investment of about $2.4 trillion per year in clean energy and low-carbon activities. Though not astronomical, $2.4 trillion is not a small figure, equivalent to 2.5% of global annual GDP.

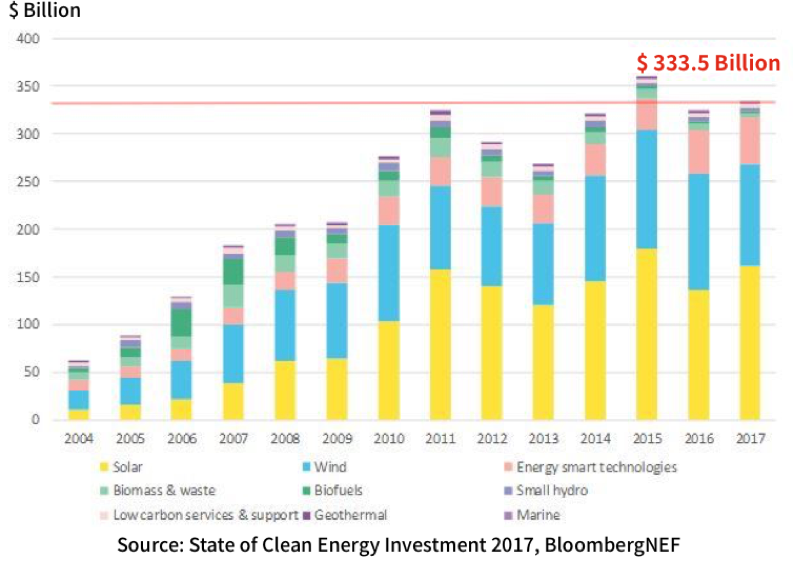

At present, the world’s total investment in climate mitigation is about $330 billion per year, only 14% of the $2.4 trillion target. However, the investments in clean energy have rapidly grown over the past decade, which gives us a reason to be confidence. Figure 2 shows that since 2004, the global investment in clean energy has increased rapidly, reaching $333.5 billion in 2017, a 5,400% increase over 14 years. This growth occurred primarily in the development of solar and wind energy and low carbon technology.

Figure 2 Global clean energy investment 2004-2017

Another study on climate finance shows that the global investment in climate mitigation and adaptation was $38.3 billion in 2016, of which over 60% came from the private sector [2]. Apparently, public funds alone will not be enough to fully tackle climate change; private finance must play a major role. More specific and proactive financial policies and financial instruments should be designed to encourage private investments to flow into green and low-carbon projects.

Retail banking can be a force of private finance to support climate mitigation. Retail banks are commercial banks providing financial services to individuals and small/micro businesses. The emerging financial technology companies (Fintech) can also be included in this category, if providing such similar services as savings deposit, wealth management, credit cards, and loans. The current global retail banking assets amount to $111 trillion [3]. Therefore, the retail banking industry can become an important source of climate finance.

An additional benefit of leveraging retail banking for climate mitigation is the industry’s ability to influence public behavioral change, as its customers are individuals, households, and small businesses. The retail banking business has significant potential to promote low-carbon behaviors through its close business interactions with general public.

China’s commercial banking sector is the largest in the world by assets. Four of the world’s top five largest banks are China owned: the Industrial and Commercial Bank of China, the China Construction Bank, the Agricultural Bank of China, and the Bank of China [4]. Since 2009, the retail banking revenue of Chinese commercial banks has grown by an average of 23% per year and is expected to reach 3.2 trillion Chinese yuan (CNY) in 2020 (about US $470 billion). China is now the world's second largest retail banking market after the United States [5]. Currently, only a small portion of this asset pool is explicitly invested in addressing climate change.

In 2016, China’s seven central government ministries jointly issued Guidelines for Establishing the Green Financial System. Since then, more policies concerning green finance have been rolled out, including on green credits, green stock indices, green bonds, green business guarantee, green development funds, information disclosure by public listed companies, compulsory environmental liability insurance, and environmental impact assessments [6]. These governmental measures have placed China in a leading position in the world on green finance, especially regarding the size and growth of green credit and green bonds. In 2017, China issued 248 billion CNY (about US $37 billion) worth of domestic and overseas green bonds, which was 7.3% increase over that of 2016 and 24.59% of the global green bond market [7]. A report by the Research Bureau of the People's Bank of China estimates that China's green investment demand is 3 to 4 trillion CNY per year, 85% of which will need to come from the market [8].

Despite the impressive progress, we think the scope of green finance in China can still expand, particularly to the field of personal consumption. That’s why NRDC and China’s Green Finance Committee co-organized a seminar on January 7, 2019 to discuss how green finance may promote green personal consumption in China. Chinese experts pointed out that in the past years, China’s green finance had mainly focused on large projects from large institutions, such as funding sewage treatment plants, new energy projects, and construction of subways and highspeed railways, but not yet adequately covered consumers, small and micro businesses, and the agriculture sector. They underscored the need to let green finance reach individuals and small businesses through a three-pronged approach.

1) Mainstreaming the concept of “green consumption”. In recent years, the number of people using consumer credits and loans has been increasing in China. The main purposes of those credits and loans were for home and auto mortgages, home renovation, and purchasing household appliances. Incentive policies, such as preferential credits and lower interest rates, may be designed to encourage consumers to buy or rent certified green real estate properties, low-emission vehicles, and energy-efficient appliances.

2) Creating more options of green investment and green savings. With the growing public awareness of environmental issues, the number of Chinese citizens concerned about the environment and climate change would be increasing. They will prefer to have their money invested in environmentally beneficial projects. When informed, some individuals could choose to avoid their savings supporting polluting and energy-intensive industries. Banks and financial institutions could develop green saving accounts and low-carbon wealth management products to promote individual green investments.

3) Helping small and micro businesses through green finance. At present, banks and financial institutions find it difficult in the loan review process to incorporate environmental risk and impact considerations for small business applicants due to a lack of information on their environmental records and of means to verify the businesses. Efforts should be made to increase the availability of environmental information on small and medium-sized companies, define practical standards of what constitute green companies and green projects, and encourage banks and financial institutions to give priority support to small businesses for their energy efficiency and low-carbon initiatives.

The NRDC, an international environmental nonprofit, believes green finance will play a central role in accelerating the reduction of greenhouse gas emissions. We recently launched a new project in China focusing on promoting climate finance from the retail banking industry. In this project, we will seek to collaborate with Chinese financial academic institutions, commercial banks and other partners to 1) strengthen the incentive policies for overcoming the obstacles in applying green financial instruments; 2) promote the development of green saving and green investment products and instruments, especially those that can reduce greenhouse gas (GHG) emissions, for individual customers and small businesses; 3) support the improvement of environmental information disclosure mechanisms and standards, particularly information on GHG emissions reduction, and clearly define “low carbon” and “green” in the finance context to help banks and customers make choices; 4) enhance public awareness and confidence in green financial products; and 5) facilitate international exchanges in green finance and the related capacity building.

For climate safety and sustainable development, NRDC looks forward to contributing to the advancement of green finance in China, particularly in the retail banking sector through our current project.

——————————————

[1] IPCC is the Intergovernmental Panel on Climate Change.

[2] “Global Landscape of Climate Finance”, Climate Policy Initiative (2017).

[3] “A Year in Review and What’s Ahead for Our Climate Finance Strategy” , Marilyn Waite (2018).

[4] “2018 Global Market Intelligence”, Standard & Poor's (2018).

[5] “Intensive and Intelligent Leaping: The Road to Developing Retail Banking”, McKinsey (2017).

[6] Such as the “Opinions of the CPC Central Committee and the State Council on Accelerating the Ecological Civilization Construction” (April 25, 2015), “Overall Plan of Ecological Civilization System Reform " (September 11, 2015); " Guidelines for Establishing the Green Financial System " (August 31, 2016) and so on.

[7] “China Green Bond Market Development Report (2018) ”, Green Finance International Research Institute, Central University of Finance and Economics.

[8] “China Green Finance Development Report 2017”, Research Bureau of the People's Bank of China (2018).